How to check BI Checking from application and IDEBKU OJK

Did you know that every loan you have ever applied for is recorded in a system? This system is called BI Checking now officially known as the Financial Information Service System (SLIK), operated by the Financial Services Authority (OJK).

In Indonesia, BI Checking plays a decisive role in determining whether a loan application at a bank or financing institution is approved or rejected. Beyond that, it also influences the credit limit and interest rate you receive.

What Is BI Checking?

BI Checking is a system that records all credit transactions belonging to every Indonesian citizen. The data captured includes the borrower's identity, collateral provided, and payment history (collectibility).

As a borrower, you can perform a personal BI Check to view your own credit score. Banks and financial institutions can also access this data to determine loan limits, review credit scores, and assess a prospective borrower's repayment capacity.

If your credit payment history is clean and on time, obtaining new credit becomes easier. Conversely, if you frequently miss credit card or buy-now-pay-later (paylater) payments, your collectibility score may decline and future loan applications risk being rejected.

The Difference Between BI Checking and SLIK OJK

Many people still use the term "BI Checking," even though the official name changed in 2018. Here is a full explanation:

Conclusion: BI Checking and SLIK OJK refer to the same system. The term "BI Checking" is no longer official but remains widely used. To check your credit history, use the SLIK OJK portal at idebku.ojk.go.id.

Components of the SLIK OJK Report

When you receive your iDeb (Debtor Information) report from OJK, it will contain five main components:

1. Debtor Identity Data

Contains personal information such as your full name, date of birth, address, National ID number (NIK), Tax ID number (NPWP), and your mother's maiden name. This is used to verify the identity of the credit applicant.

2. Credit or Financing Data

Displays all loans you currently have or have previously held, whether from banks or other financing institutions. This includes loan amounts, tenors, interest rates, and outstanding installment balances.

3. Payment History (Credit Collectibility)

This is the most critical section. It shows how consistently you have been making repayments. There are five collectibility categories, which will be discussed in the next section.

4. Guarantor Data (If Applicable)

Shows whether you have ever served as a guarantor for another person's loan. If the primary borrower defaults, the guarantor's credit record may also be affected.

5. Additional Information Includes the date of the most recent data update, the total credit ceiling across all accounts, and additional notes from the relevant financial institution.

How to Check BI Checking Online in 2026

There are two ways to perform a personal BI Check: visiting an OJK office in person, or doing it online from home via the portal idebku.ojk.go.id.

Online via idebku.ojk.go.id

- Prepare your documents. Indonesian citizens need their electronic National ID (e-KTP). If applying on someone else's behalf, also include a power of attorney.

- Go to idebku.ojk.go.id.

- Click "Registration" on the homepage.

- Fill in your personal details as listed on your ID, including an active email address and phone number.

- Check quota availability. If a session slot is available, you will be prompted to complete additional data. If fully booked, you will receive a notification with the next available service schedule.

- Upload your documents: a photo of your original e-KTP and a selfie holding your ID card, following the on-screen instructions.

- Check the data accuracy declaration, then submit.

- Check your email. You will receive a registration number from OJK.

- Your report will be sent to your email within a maximum of one business day (1x24 hours).

To monitor your registration status, visit idebku.ojk.go.id and select the "Service Status" menu.

Offline (Walk-in to OJK Office)

Visit your nearest OJK office Monday through Friday, from 09:00 to 15:00, and bring:

- Your original e-KTP and a photocopy

- An iDeb request form (available at the OJK office)

How to Read Your BI Checking Results

After registering, you will receive an email from OJK containing a PDF file of your iDeb report. Here is how to read it:

- Step 1: Open the PDF file from the OJK email. Check your spam folder if it does not appear in your inbox.

- Step 2: Locate the "Collectibility" or "Credit Quality" section of the report. This is where your credit status is recorded.

- Step 3: Read the "Credit Quality Code" column:

- 1 = Current (best)

- 2 = Under Special Attention

- 3–5 = Problematic (risk of new credit applications being rejected)

- Step 4: Verify that all credit data listed is accurate. If any information is incorrect, for example a loan you have already paid off is still listed as active, you may submit a correction request to OJK with proof of repayment.

- Step 5: Pay attention to the "Data Update Date" column. SLIK data is updated monthly by each financial institution.

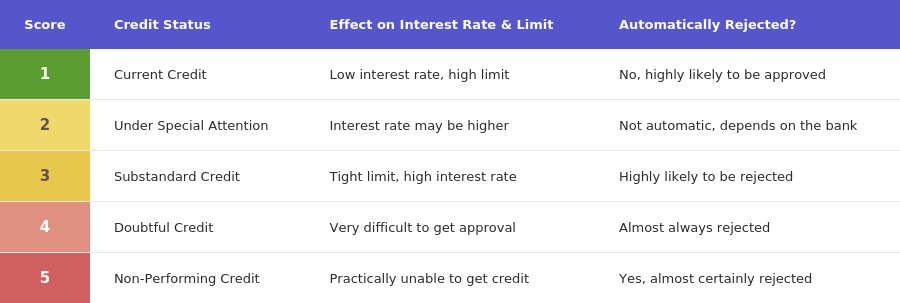

Credit Score Criteria in BI Checking (Collectibility 1–5)

A borrower's repayment track record is translated into a collectibility score with five levels:

The higher the collectibility score (3–5), the harder it becomes to obtain new credit, as banks must assume a greater level of risk.

The Impact of BI Checking on Credit Applications

Many people wonder: how much does a BI Checking score actually affect their loan application? Here is the answer:

1. Determines credit approval or rejection

Banks use the collectibility score as one of their primary evaluation criteria. Applicants with a score of 1 have a significantly higher chance of approval compared to those with a score of 3 or above. However, a score of 2 does not automatically result in rejection, as each bank has its own internal policies.

2. Affects interest rates and credit limits

Borrowers with a clean credit history (score 1) tend to receive lower interest rate offers and higher credit limits, as banks consider them low-risk borrowers.

3. Determines how far back banks look

In general, banks focus primarily on the last 2–3 years of credit history. This means that a non-performing loan from more than 3 years ago that has since been fully repaid typically has minimal impact on a current credit decision.

4. Applies to all types of credit

From mortgages (KPR) and personal loans (KTA), to credit cards and OJK-registered online loans, all are checked through the SLIK system at the time of application.

How to Repair a Poor BI Checking Score

If your BI Checking result shows a score of 3, 4, or 5, do not panic. There are concrete steps you can take:

1. Pay off outstanding debt as soon as possible

This is the most important step. As long as active arrears remain, your credit score will not improve. Prioritize paying off the longest overdue credit first.

2. Request a data update after repayment

Once the debt is settled, ask the relevant financial institution to update your credit status in the SLIK system. This process typically takes 1–3 months before the data is refreshed.

3. Build a new, positive credit history

After clearing your arrears, start establishing a new track record. Apply for a small credit product such as a credit card with a low limit, then pay the bill on time every month. Maintaining consistency for 6–12 months will gradually improve your credit profile.

4. Manage your Debt-to-Income (DTI) ratio

Ideally, your total monthly installments should not exceed 30% of your fixed income. If you earn Rp5,000,000 per month, aim to keep total repayments below Rp1,500,000 per month.

5. Monitor SLIK regularly

Check SLIK OJK at least every 3–6 months to ensure your data is being updated correctly and that there are no recording errors.

How long does credit score recovery take? Generally, it takes 12–24 months to recover a credit score from poor (score 3–5) to current (score 1), provided there are no new arrears and all payments are made on time consistently.

Tips for Maintaining a Good Credit Score

Prevention is always easier than correction. Here are six tips for keeping your credit score healthy:

1. Always pay bills on time.

Even a single day's delay can be recorded in the SLIK system and drop your status to DPK (score 2). Enable auto-debit or set payment reminders to avoid missing due dates.

2. Avoid having too many active loans at the same time

Multiple concurrent credit lines signal higher risk to banks. Pay off one loan before applying for another.

3. Use credit cards wisely

Aim to keep your credit card usage below 30–40% of your total credit limit. Utilization close to 100% signals dependence on debt.

4. Maintain a healthy debt-to-income ratio

Total monthly installments should ideally not exceed 30% of your income, which is the standard most banks use when assessing creditworthiness.

5. Check your credit score regularly

Checking SLIK OJK yourself does not affect your credit score (unlike a hard inquiry made by a bank when processing a loan application). Do this every 3–6 months to catch data errors early.

6. Avoid applying for new credit too frequently

Each application is recorded in the system. Submitting too many applications in a short period of time may be interpreted as a sign of financial instability.

What Can You Do in the Honest App?

1. Check Your Credit Score Directly from Your Phone

Monitor your credit health anytime, anywhere. No need to register at idebku.ojk.go.id or wait for an email — you can instantly view your credit score right from the Honest app.

{{alert-cta}}

2. Apply for the Honest Credit Card in 5 Minutes

If your credit score is in good shape, you can apply for the Honest Credit Card directly within the same app. The application process is 100% online, takes only 5 minutes to complete, and approval can be received within 2 hours.

3. Build a Healthy Credit History

The Honest Credit Card is the ideal tool for establishing a positive credit history. Use it for everyday transactions, pay your bills on time each month, and watch your credit score steadily improve.

Honest Credit Card Advantages:

Frequently Asked Questions (FAQ) About BI Checking:

1. Are BI Checking and SLIK OJK the same thing?

Yes, both refer to the same system. SLIK OJK is the latest official name, which replaced BI Checking in 2018. The difference lies in the managing authority (previously Bank Indonesia, now OJK) and the broader data coverage under SLIK.

2. How long does it take to receive BI Checking results after registering online?

After completing your registration at idebku.ojk.go.id, your iDeb report will be sent to your email within a maximum of 1x24 hours (one business day). Make sure the email you registered is active and check your spam folder.

3. Can BI Checking data be deleted?

Data in SLIK is historical and cannot simply be erased. However, the impact of a poor credit history diminishes over time, especially if you maintain consistent, on-time payments. Banks generally focus on the most recent 2–3 years of credit history.

4. How do I fix a bad credit score?

The main steps are: pay off all outstanding debt, ask the financial institution to update your data in SLIK, build a new credit history through small credits paid on time, and be patient, as this process takes 12–24 months.

5. Does checking my own BI Checking affect my credit score?

No. Checking SLIK OJK yourself has absolutely no impact on your credit score. This is different from a hard inquiry conducted by a bank when processing a loan application. You can check anytime without concern.

6. Does a score of 2 (DPK) automatically lead to rejection when applying for credit?

Not automatically. A score of 2 means there has been a delay of 1–90 days, but each bank has different policies. Some banks still accept applicants with a score of 2, depending on the type of credit, loan amount, and the applicant's overall financial condition.

7. How long does it take to recover from a BI Checking score of 5?

From a score of 5 (non-performing loan), recovery typically requires a minimum of 24 months after all arrears are fully repaid and the data is updated in the SLIK system. Consistent, on-time payments throughout this period are critical to the recovery process.

This article was compiled based on official information from the Financial Services Authority (OJK) and updated in April 2026. For the latest information, visit the OJK website or idebku.ojk.go.id.

What are you waiting for?

Get your Honest Card today